Affordable Options for Individual Owners and Small Family Offices

Managing mineral and royalty interests shouldn’t require a special diploma or a corporate-sized tech stack. If you’re an individual owner or part of a small family office, you likely want tools that simplify tracking your interests, without the steep costs and complexity of enterprise systems.

Luckily for our readers, we have compiled a list of several affordable, intuitive software platforms designed specifically with private mineral owners in mind.

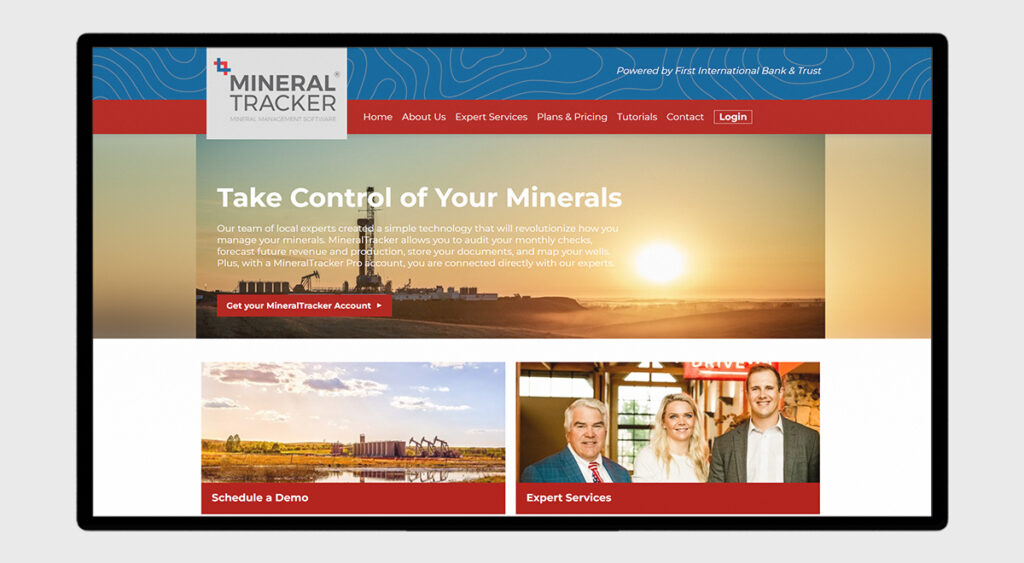

1. MineralTracker

Best for: Hands-on tracking and check reconciliation

Website: mineraltracker.com

MineralTracker was built by mineral owners, for mineral owners. With this piece of software you can monitor production, track your income and ensure your royalty checks are accurate, all from a cloud-based and user-friendly dashboard.

Pricing tiers are based on individual owners, and they also offer a free demo to allow you to explore before committing.

Key features:

- Track wells and production volumes

- Reconcile monthly royalty payments

- Visualize income trends over time

- Store ownership documentation securely

Why we like it: It’s tailored for individuals and small portfolios—not corporations.

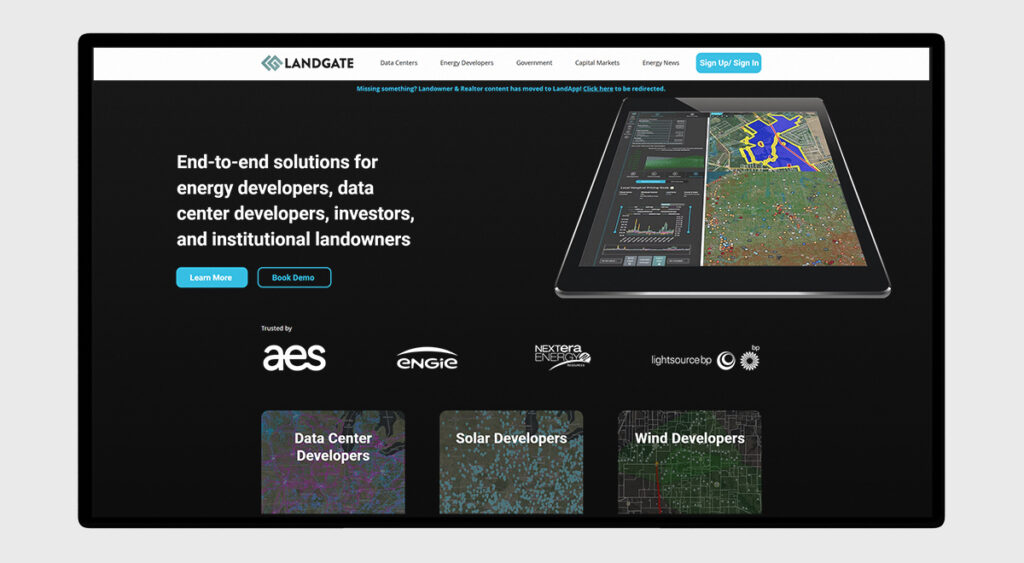

2. LandGate (LandApp)

Best for: Valuation and market visibility

Website: landgate.com

LandGate’s LandApp isn’t just for sellers, it’s also a valuable platform for mineral and landowners who want to track their assets, explore leasing opportunities, or estimate value. Many features are free or low-cost, making it a smart add-on for owners curious about their portfolio’s true worth.

Key features:

- View mineral, solar, and wind rights

- Track market interest and property data

- Access valuation reports

Why we like it: Adds market intelligence to your toolbox, even if you’re not looking to sell.

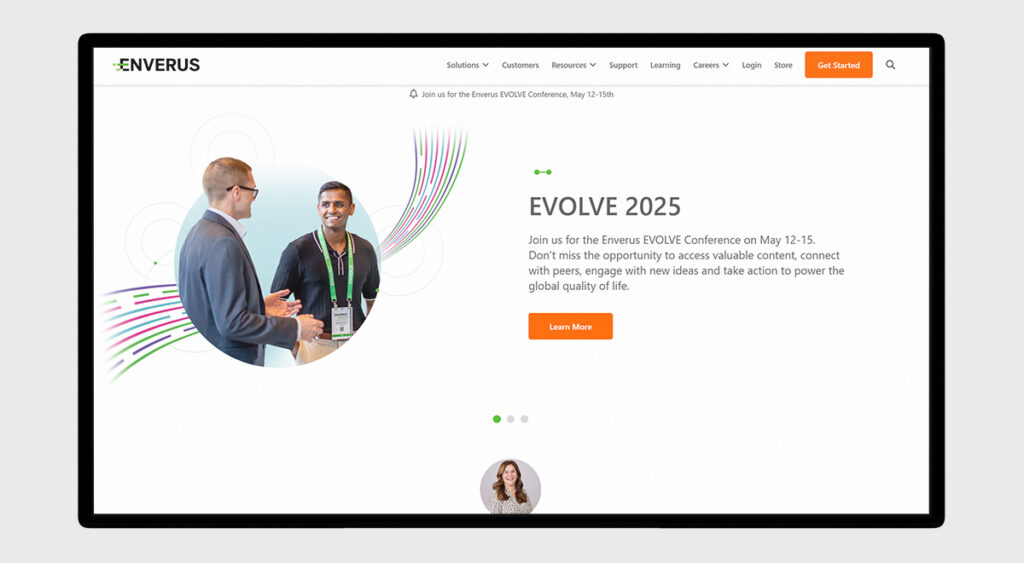

3. Enverus Owner Relations (Formerly EnergyLink)

Best for: Accessing operator data and check details

Website: enverus.com

While Enverus is widely known for its enterprise products, its Owner Relations portal, formerly known as EnergyLink, is a useful tool for individual owners whose operators participate in the platform. It provides access to check stubs, production data, and reports, helping you cross-check payments and stay informed.

Key features:

- Online access to royalty statements

- Operator production data

- Document download and reporting

- Free to use if your operators participate

Why we like it: Many operators already use Enverus—you just need to activate your account.

4. Trellis Energy

Best for: Simplified royalty income tracking

Website: trellisenergy.com

Trellis offers an approachable royalty management tool that helps you understand what you’re owed and when you’ve been paid. Built for non-technical users, this platform is perfect for owners who want clear, concise insights into their royalty income.

Key features:

- Reconcile check payments

- Forecast future revenue

- Organize tax data and year-end reports

- Understand deductions and pricing

Why we like it: Designed for small portfolios and owners who want clarity without the learning curve.

How to Choose the Right Platform

If none of the above tools meet your needs, there are numerous other options available with basic Internet research. However, while comparing tools, it’s important to consider:

- Size of your portfolio: Most tools discussed here cater to owners managing under 100 wells. Larger portfolios may require more enterprise-oriented solutions.

- Support and onboarding: Choose platforms that help you get started.

- Ease of use: Look for simple dashboards and strong customer reviews.

- Pricing transparency: Avoid tools that hide pricing / fees behind sales calls. These are nearly always enterprise solutions and too pricy for smaller mineral owners.

Get Help from Allegiance

Still unsure where to start? At Allegiance Oil & Gas, we help individual owners and family offices navigate mineral ownership with clarity. Whether you need tool recommendations, help with interpreting your royalty checks, or support with lease management, we’re here for you.

Disclaimer: Allegiance Oil & Gas is not affiliated with the software providers listed above. These recommendations are based on publicly available information and feedback from individual owners we have worked with.