For many mineral owners, nothing is more frustrating than seeing a well on file, hearing that production has started, or expecting a royalty check — only to find out the money is not being released. In the oil and gas world, that situation is often described as payments being “in suspense” or “suspended.”

That phrase can sound alarming, but it does not always mean something is seriously wrong. Sometimes the issue is as simple as an outdated mailing address or an unsigned division order. Other times, the payor is waiting on probate documents, title curative, taxpayer information, or clarification about who should be paid. In some cases, there is not actually a suspense problem at all — the account balance may simply be below the operator’s minimum check threshold, or the funds may have already been transferred to a state’s unclaimed-property program.

The key is not to assume. Mineral owners who understand what suspended royalties usually mean can ask better questions, gather the right documents, and often resolve payment delays much faster. Below is a practical guide to the most common causes of suspended royalties and the first things to check before the problem drags on for months.

What Suspended Royalties Usually Mean

At a basic level, suspended royalties are proceeds that have been earned but not yet released to the owner. The well may be producing, revenue may be coming in, and the payor may even have calculated what belongs to your interest. But instead of sending a check or ACH payment, the payor holds the funds until a specific issue is resolved.

That issue may be administrative, legal, or title-related. The important thing to understand is that suspense is usually tied to the payor’s need for clean payment instructions. If the operator or purchaser is not comfortable that the right person is being paid in the right amount, the funds are often held until the records are corrected.

This is one reason suspended royalties frequently appear after inheritance, trust changes, divorce, deed transfers, returned mail, or ownership questions. As we discussed in our recent post about division orders, payment paperwork matters more than many owners realize. Suspense is often the result of a mismatch between the owner’s actual interest and the payor’s records.

The Most Common Reasons Royalty Payments Get Held Up

1. Ownership has changed, but the payor’s records have not

One of the most common causes of suspense is an ownership change that never made its way cleanly into the payor’s system. This happens often when an owner dies, minerals are inherited by several heirs, a trust or LLC is created, or a portion of the interest is sold or gifted.

From the owner’s point of view, the family may know exactly who should receive the money. From the payor’s point of view, however, the last verified owner may still be a deceased individual or an outdated entity name. Until probate paperwork, deeds, affidavits, trust documents, or other transfer materials are reviewed and accepted, the payor may suspend the account rather than risk paying the wrong person.

2. The payor is missing address, tax, or banking information

Not every suspense problem is legal. Sometimes the payment is delayed because the payor cannot confidently deliver the funds or issue year-end tax reporting. A bad mailing address, returned check, missing W-9, or incomplete direct-deposit setup can be enough to trigger a hold.

This is especially common after a move, a name change, or a period of inactivity. Owners sometimes assume that if one operator has the right information, every operator will too. In reality, each payor maintains its own records, and an update with one company does not automatically update the others.

3. A division order has not been returned or does not match the file

Division orders are designed to confirm who should be paid and at what decimal interest. If the form is never returned, is signed incorrectly, or conflicts with the payor’s title setup, payments can be delayed while the file is reviewed.

Owners should not rush to sign a division order without reviewing it, but they also should not ignore it. When a division order is sitting unanswered, suspense can follow. If the form appears wrong, the goal is not simply to refuse it — the goal is to identify what is wrong and start the correction process with supporting documents.

4. There is a title issue, adverse claim, or decimal-interest dispute

Sometimes the problem is more substantive. The payor may have a title requirement that was never satisfied, a deed may contain an ambiguity, multiple parties may be claiming the same interest, or the decimal interest may not line up with the lease, unit, or chain of title. In those situations, the payor may suspend all or part of the proceeds until the title issue is cured.

This is where owners often get frustrated, because the well may clearly be producing while the money remains stuck. But from the payor’s perspective, suspense is a risk-control decision. Releasing funds too early can create a much larger problem if the ownership later proves incorrect.

5. The account has not reached the minimum payment threshold

Owners sometimes describe a missing check as a suspense problem when the real issue is simply the payor’s check threshold. If revenue has accrued but has not yet reached the minimum amount required for a payment cycle, no check may be issued that month.

That distinction matters. True suspense usually means the funds are being held because something needs to be fixed. A threshold hold, by contrast, may simply mean the account balance has not yet reached the amount at which the payor regularly cuts checks. If the property is small or production is light, this can make payments look irregular even when nothing is actually wrong.

6. The funds have been sitting long enough to move toward unclaimed property

If a royalty issue goes unresolved for too long, the funds may not stay with the payor forever. Depending on the state and the circumstances, suspended proceeds or uncashed checks can eventually be remitted to a state unclaimed-property division. At that point, the problem shifts from getting the operator to release funds to recovering the money from the state.

This is one reason old addresses and deceased-owner accounts should be addressed quickly. A payment issue that looks minor in the beginning can become more time-consuming once due-diligence letters, state reporting deadlines, and claim forms enter the picture.

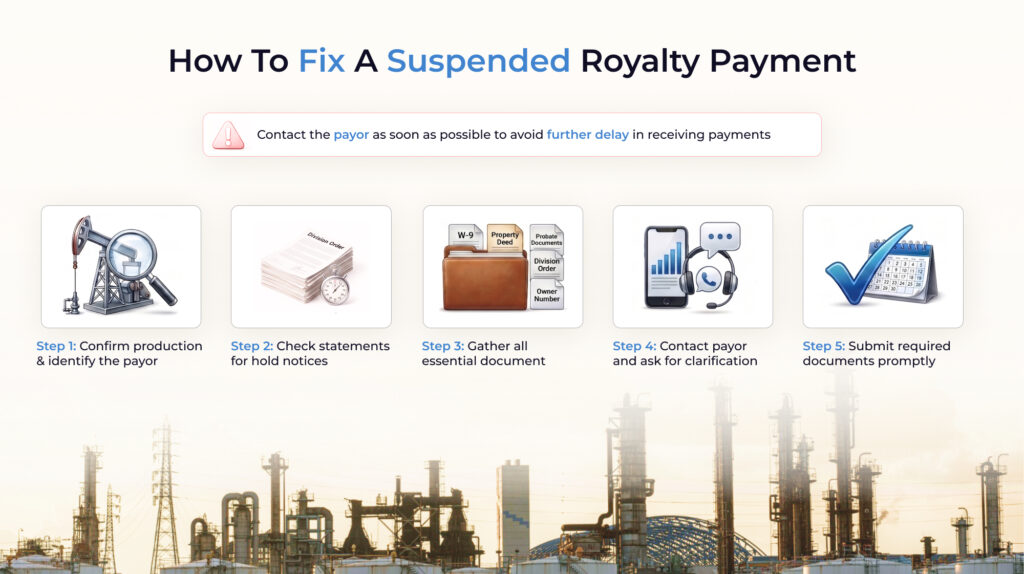

What Mineral Owners Should Check First

Before assuming the payor is doing something improper, it helps to work through a short checklist. In many cases, the answer becomes clearer once you verify a few practical items.

- Confirm the well or property is actually producing and that the company you are contacting is the payor responsible for your revenue.

- Review your most recent check stub, revenue statement, division order, or owner portal for any suspense code, hold notice, or comments tied to the account.

- Make sure your name, mailing address, ownership entity, and taxpayer information are current with that specific payor.

- Ask whether the account is suspended for title, probate, transfer, division-order, or tax-reporting reasons — or whether the balance is simply below the minimum payment threshold.

- If ownership changed, confirm what exact documents the payor still needs rather than sending a general stack of papers and hoping for the best.

- If the owner is deceased, ask whether payments are suspended at the owner level, the property level, or only on the affected interest.

- If no recent payments have been received, ask whether any funds have already been reported to unclaimed property.

Documents to Have Ready Before You Contact Owner Relations

The fastest owner-relations calls usually happen when the owner has the right information in front of them. Calling to say “my check never showed up” is understandable, but it often leads to a slow back-and-forth if the representative has to start from zero.

Before reaching out, gather as many of the following items as you can:

- Owner number, payee number, or account number from a prior statement or 1099

- Well name, lease name, property name, county, and state

- A copy of the division order, if one was issued

- Recent revenue statements or check stubs

- Probate, deed, trust, LLC, or transfer documents if ownership changed

- Death certificate and estate documents if the prior owner has passed away

- Completed W-9 and any address-change or ACH forms the payor requested

- Any suspense or due-diligence letters you have received

The goal is to make the conversation specific. Instead of asking why you have not been paid, you want to be able to ask whether the account is being held for title, transfer, address, tax, division-order, threshold, or unclaimed-property reasons. That tends to produce much clearer answers.

Reach Out To The Payor

When you speak with owner relations, try to leave the conversation with something more concrete than “it is under review.” The most useful questions are the ones that narrow the issue and force the next step to become clear.

- Is the account actually in suspense, or is the balance just below the payment threshold?

- If it is suspended, what is the exact suspense reason shown in your system?

- Is the hold tied to the owner, to a specific property, or to the entire account?

- What documents are still needed to release funds?

- Have you already sent a due-diligence or deficiency letter, and if so, when?

- Once the documents are accepted, will prior suspended funds be released automatically?

- Have any funds already been turned over to state unclaimed property?

When the Problem Is Bigger Than a Simple Paperwork Fix

Some suspense issues do not resolve with a quick form submission. If there is a title dispute, a missing probate proceeding, conflicting deed language, or a serious decimal-interest disagreement, the matter may require title review or legal work before the payor will release funds.

That does not necessarily mean litigation is coming. But it does mean owners should avoid guessing. Sending incomplete or inconsistent documents can slow the file even further. In those situations, it often makes sense to organize the title history first, understand exactly what interest is being claimed, and then decide whether a land professional, title specialist, attorney, or experienced mineral buyer should be involved.

How This Connects to the Bigger Ownership Picture

Suspended royalties are rarely just a payment problem. More often, they are a signal that something in the ownership record needs attention. That is why owners dealing with suspense frequently discover related issues involving inheritance paperwork, missing deeds, fractional ownership splits, outdated division orders, or incorrect assumptions about what type of interest they actually own.

In other words, suspense can be a nuisance — but it can also be a useful warning sign. If a payor has trouble paying your account cleanly today, that same problem may also affect future payments, future tax reporting, or even the marketability of the interest if you later decide to sell.

How Allegiance Oil & Gas Helps

At Allegiance Oil & Gas, we regularly speak with mineral and royalty owners who are trying to make sense of delayed payments, ownership questions, and incomplete records. In many cases, the real issue is not just the missing check — it is uncertainty about what the owner actually has, whether the file is clean, and what steps should come next.

Our team helps owners think through the practical side of the problem. That may involve reviewing documents, identifying likely title or transfer issues, helping owners understand how suspended funds fit into the larger value of the asset, or simply clarifying what questions to ask before a payment delay turns into a long-term headache.

Final Thoughts

Suspended royalties can feel like money disappearing into a black box, but the cause is often more understandable once you break it down. Start by confirming whether the issue is true suspense, a minimum-payment threshold, a paperwork problem, or an ownership change that never got fully processed. Then gather your documents, ask direct questions, and work from the specific suspense reason rather than from assumptions.

The sooner the real issue is identified, the easier it usually is to resolve. And if the problem points to a larger ownership or title concern, dealing with it now can save far more trouble down the road.

Disclaimer: This article is for general informational purposes only and is not legal or tax advice. Royalty-payment rights and suspense procedures can vary by state, lease, operator, and ownership history. Owners should consult qualified legal or tax professionals for advice on their specific situation.